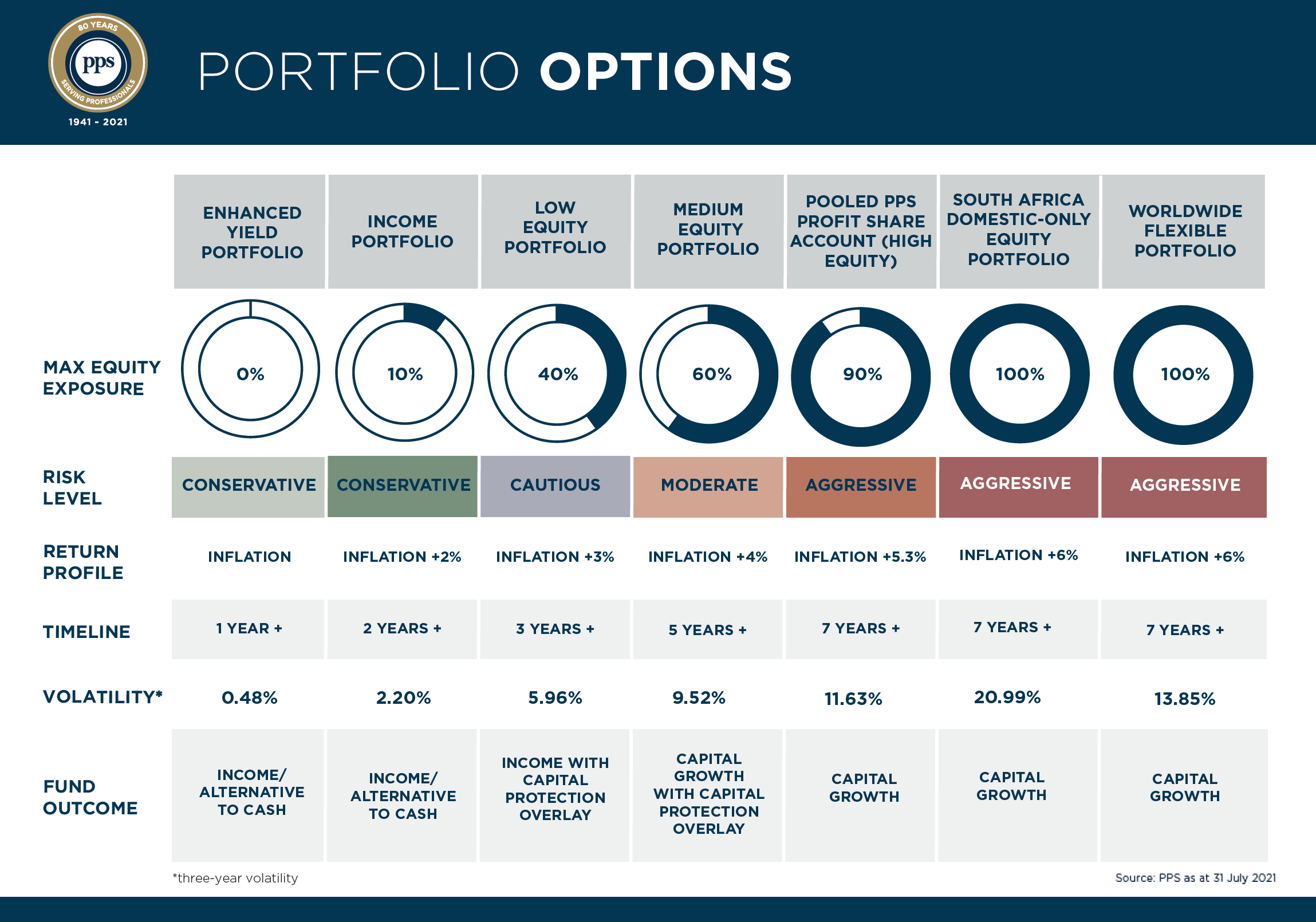

PPS Portfolio Choice

Before reaching retirement – from the age of 55 – PPS offers you the opportunity to start aligning how your PPS Profit-Share Account is invested to align to your retirement plan via the Portfolio Choice.

For more information on the PPS Profit-Share Account Portfolio Choice:

Read - Member Brochure (PDF)

Watch the video - https://youtu.be/KIajotajIuc

For more information on the Portfolio Choices:

Watch the video - https://youtu.be/EeOekUusyFA

Critical Illness/or Severe Illness

To submit a claim under PPS Critical Illness Cover or Severe Illness Cover, the following forms are required:

- PPS Critical Illness and Severe Illness claim form – Member.

- PPS Critical Illness and Severe Illness claim form – Doctor.

Please note:

- Separate claim forms apply for Professional Health Preserver and Education Cover Illness benefits.

- All claim forms must be accompanied by a comprehensive medical report and copies of any diagnostic tests confirming the diagnosis.

Critical Illness/or Severe Illness

Claims under CatchAll Cover will be considered when the life-insured suffers a serious medical or physical condition that is permanent and unlikely to improve, even with further medical or surgical treatment. The condition must not be listed under any other benefit category. To qualify, the life-insured must score at least 11% on the Whole Person Impairment (WPI) scale, which is based on guidelines from the American Medical Association. The benefit is paid in tiers of 50%, 75% or 100%, depending on the WPI score obtained.

Critical Illness/or Severe Illness

A survival period will be applied to the dread disease and impairment condition you are claiming for. You must be alive at the end of the survival period to receive a benefit payment. If you die during the survival period, no benefit payment will be made since you would not have incurred the lifestyle adjustment costs resulting from the dread disease or impairment condition which the product is designed to cover.

Please note:

- A 14-day general survival period always applies.

- Certain conditions have longer survival periods built into the definitions to determine the permanence or severity of the condition.

- Heart attack has a 30-day survival period.

- Stroke has a three-month survival period.

Critical Illness/or Severe Illness

This will be based on your doctor's assessment of the medical information submitted against the definitions/degrees of each level as defined in your policy document.

Critical Illness/or Severe Illness

It is the degree of severity of your illness based on the definitions in the PPS Provider™ Policy. Refer to your policy certificate and document for these criteria.

Critical Illness/or Severe Illness

The award will depend entirely on the information submitted with your claim and the stage of the disease that you are suffering from. If you are awarded a 25% benefit and your condition worsens, you may submit a new claim and additional reports, which PPS will consider. A further benefit will be paid if your condition meets the definition for a higher severity level.

Critical Illness/or Severe Illness

The amount paid depends on the severity of the condition and the benefit option selected, as defined in the policy document. If the condition qualifies for a 100% award, the full sum assured will be paid. If the award is less than 100%, the benefit will be paid as a percentage of the sum assured according to the severity level:

- Severity level A – 100% of the sum assured.

- Severity level B – 75% of the sum assured.

- Severity level C – 50% of the sum assured.

- Severity level D – 25% of the sum assured.

Members who have selected the Core 100% benefit will receive 100% of the sum assured for the following conditions, provided the claim qualifies for at least a severity level D:

- Heart attack (cardiovascular).

- Cardiac surgery and procedures (cardiovascular).

- Stroke (neurological).

- Cancer.

All other conditions will be paid based on their severity.

Members who have selected the Critical Illness 100% (CO 100%) benefit may qualify for a 100% payment for most conditions listed in the definitions, provided the claim qualifies for at least a severity level D. Some conditions, such as Group 1 prostate cancer, may be paid at a lower percentage based on severity.

Critical Illness/or Severe Illness

Yes, you can only be paid 100% (100% in total for the accelerated PHP) of the insured amount for each condition covered under your policy. The standalone cover remains in force for unrelated conditions for which you can continue to claim should an unrelated event occur. The event paid for will be excluded from future claims if paid at 100% of the benefit.

Critical Illness/or Severe Illness

The process should not take more than eight working days to finalise once all the required information has been received. However, the process will take longer if additional information is required or the standard forms have not been completed correctly.

Critical Illness/or Severe Illness

The assessor may request additional information to determine the severity of your illness or when your illness started.

Critical Illness/or Severe Illness

Yes, additional information may be requested from you or your treating doctor. This information will only be requested if sufficient information is not available to assess your claim.

Critical Illness/or Severe Illness

The costs of the initial report will be for your account. PPS will cover the cost of any additional independent specialist reports required.

Critical Illness/or Severe Illness

When you are diagnosed with any of the conditions listed in your policy document.

Life Cover FAQ

The remaining half of the life cover sum assured will be paid on death as described above.

Life Cover FAQ

The premiums that you are paying will be reduced accordingly in line with the remaining sum assured.

Life Cover FAQ

The benefit payable will be half the life cover sum assured at the time of claim.

Life Cover FAQ

This benefit is payable if you are diagnosed with a terminal illness (as specified by PPS Insurance) and are likely to die within the next 12 months.

Life Cover FAQ

Yes, a Terminal Illness benefit is automatically included with your Life Cover.

Life Cover FAQ

The exact same process as above will apply. However, no immediate needs can be paid from the PPS Profit-Share Account™. It can also not be ceded.

Life Cover FAQ

The full life cover insured amount as at the date of death will be paid based on the beneficiary nomination form, unless the policy was ceded (security for a loan). In these instances, the cessionary will be paid first and the remainder, if any, will be paid to the beneficiary(ies) based on the nomination form.

Life Cover FAQ

The claim should be paid within four working days from the receipt of all the requested information.

Life Cover FAQ

The assessor may request additional information to determine when the illness leading to the death started (depending on the condition claimed).

Life Cover FAQ

A request for “Immediate needs” (R100 000) may be submitted to PPS at [email protected] with a copy of the death certificate, beneficiary(ies) banking details, including proof thereof (a bank letter not older than three months) and ID of the beneficiaries.

PPS will pay the Immediate Needs benefit within two working days upon receipt of all documents.

Life Cover FAQ

Notification of death should be sent to [email protected] with a copy of the death certificate and exact cause of death. The relevant documentation will be forwarded to the person submitting the claim.

Life Cover FAQ

From the Master of the High Court.

Life Cover FAQ

Natural death | Unnatural death |

|---|---|

Death certificate | Death certificate |

Detailed death certificate (BI 1663), if the death certificate does not indicate the exact cause of death. | Detailed death certificate (BI 1663), if the death certificate does not indicate the exact cause of death. |

Banking details of the estate or nominated beneficiary(ies). | Banking details of estate or nominated beneficiary(ies). |

A letter of executorship if paying to the estate. | A letter of executorship if paying to the estate. |

Copy of the beneficiary(ies)’s ID. | Copy of the beneficiary(ies)’s ID. |

Copy of the divorce order and settlement agreement if the deceased was divorced. | Copy of the divorce order and settlement agreement if the deceased was divorced. |

Medical report from treating doctor. | Police report (post mortem). Medical report from treating doctor. |

A copy of the Trust deed and a letter of authority of trustees if a Trust is nominated. | A copy of the Trust deed and a letter of authority of trustees if a Trust is nominated. |

Life Cover FAQ

The benefit will be paid to the minor child’s legal guardian.

Life Cover FAQ

The benefit will be paid to the deceased's estate.

Life Cover FAQ

PPS Insurance will pay the sum assured due in respect of the benefit to the cessionary, nominated beneficiary(ies) or estate if the life-insured dies during the benefit term.

The PPS Professional Disability Provider™ Product (PDP)

The benefit amount is reflected on your PPS Policy Certificate. You can also ask your PPS-accredited financial adviser for this information.

The PPS Professional Disability Provider™ Product (PDP)

Yes, once the full sum assured has been paid, the benefit ends.

The PPS Professional Disability Provider™ Product (PDP)

It will depend on whether or not we have enough information to assess your claim.

Once we have all the necessary information, your claim will be prepared for discussion by the Medical Officers Committee. The committee will assess your claim within 15 days of receiving the last piece of information. You will be informed via e-mail of the date on which your assessment will take place.

You will receive a letter detailing the decision on your claim within five working days of the meeting.

The PPS Professional Disability Provider™ Product (PDP)

This will assist us in ensuring that we make a fair and informed decision regarding your claim.

The PPS Professional Disability Provider™ Product (PDP)

PPS will pay for independent specialist reports.

The PPS Professional Disability Provider™ Product (PDP)

Possibly. Additional information may be requested from you or your (or your spouse’s or child’s) treating doctor once assessed by a claims assessor, especially if the claim period exceeds the number of days the illness is expected to last or with particular conditions claimed.

The PPS Professional Disability Provider™ Product (PDP)

- PPS Professional Disability Provider™ claim form – Member

- PPS Professional Disability Provider™ claim form – Doctor

- Comprehensive medical report from your treating specialist/doctor. (If possible, please include copies of all relevant test results, including blood test results and x-rays.)

The PPS Professional Disability Provider™ Product (PDP)

You can claim for this benefit when you suffer from a permanent condition (illness/injury) that may prevent you from using your professional training and knowledge to carry out your own occupation or any other occupation that someone with similar qualifications could carry out.

Sickness and Permanent Incapacity FAQ

Yes, your claim may include public holidays and weekends.

Sickness and Permanent Incapacity FAQ

If a claim extends over several months, PPS requires the following:

- A Declaration by Member (DBM) and Declaration by Doctor (DBD) form must be submitted monthly by the 25th of the month being claimed for.

- Confirmation that the member consulted their doctor in person during each month of the claim period.

Please note the following:

- Claims must be submitted monthly. Delays in submission will result in delays in the payment of benefits, as the claims management team is required to assess long-term claims regularly.

- PPS does not accept forms completed following telephonic consultations.

- The Declaration by Doctor form must be completed by a treating specialist who is appropriately qualified in the field of medicine relevant to the condition.

In some cases, such as recovery following surgery, the treating specialist may book the member off for an extended period. In these instances, the member may only be required to submit the DBM monthly. This will be determined by PPS assessors at the time of claim assessment.

Additional requirements may include:

- Progress reports or questionnaires from the attending specialist (at PPS’s cost).

- Questionnaires completed by the member to assess the impact of the condition on daily activities and professional duties.

Independent assessments arranged by PPS (at PPS’s cost).

Sickness and Permanent Incapacity FAQ

The Sick Pay Benefit calculation differs depending on whether the graduate professional is salaried or self-employed.

For salaried graduate professionals, the benefit will be limited to the greater of:

- Two-thirds of gross personal income; or

- Net of tax personal income.

For self-employed graduate professionals, the benefit will be limited to the greater of:

- Two-thirds of gross personal income plus 100% of actual business expenses prior to the claim; or

- Net of tax personal income plus 100% of actual business expenses prior to the claim.

Sickness and Permanent Incapacity FAQ

Usual professional duties are those occupational tasks which you carry out as part of your occupation prior to claim. This includes administrative duties such as sending e-mails and making telephone calls related to your business or occupation.

Sickness and Permanent Incapacity FAQ

Partial sickness refers to situations where, due to illness, you are unable to complete all your regular work tasks or fulfil your usual hours. However, you are still able to perform some of your standard duties. You may be eligible for a Partial Sick Pay benefit in such cases, after first claiming for total illness (on the seven-day waiting period). This requires that you spend part of each workday on tasks related to your normal occupation, using your established professional skills and knowledge. You must notify PPS of this change before you begin performing duties outside your usual role.

If you work on a partial basis, you can submit a claim for partial sickness, which is paid at 50% of your sickness benefit.

After a period of 728 days for the same or related condition, if you are still unable to perform your usual professional duties, you may be assessed for a Permanent Incapacity benefit.

If you have claimed partial incapacity for 728 days for the same or a related illness and are still unable to do your usual work, you may be considered for a Permanent Incapacity benefit.

This is based on the impact of an impairment on the ability to perform usual professional duties until the chosen benefit cease date is reached or until the member recovers. The award can be either 20%, 60% or 100%.

Sickness and Permanent Incapacity FAQ

- If you have the Family Responsibility Rider benefit, effective BEFORE 1 April 2017, you will be paid a benefit if your spouse or child is hospitalised for four consecutive days (including three overnight stays) or more.

- If you have the Family Responsibility benefit, effective AFTER 1 April 2017, you will receive a benefit if your spouse or child is hospitalised for at least three consecutive days (including two overnight stays).

Sickness and Permanent Incapacity FAQ

- District, regional and provincial hospitals

- Private hospitals

- Spinal rehab units

- Infectious diseases hospitals

- Rehab step-down facilities (e.g., Life Rehab)

- Step-down Institutions

- Frail care facilities

Which hospitals are not covered?

- Alcohol and substance abuse rehabilitation centres.

Sickness and Permanent Incapacity FAQ

If you elected to have the Admission Rider benefit, you will be paid an additional benefit calculated based on the number of days in hospital, multiplied by the cover amount for Admission benefits.

Sickness and Permanent Incapacity FAQ

Your benefit will depend on the sickness cover amount reflected on your remittance advice and will be calculated based on the number of days of sickness.

Sickness and Permanent Incapacity FAQ

No, there is no limit to the number of claims you can submit. However, if your claims are for the same or similar condition, or one related to an existing condition, the total claim period is limited to 728 days. At the end of the 728 days, the member will be assessed for Permanent Incapacity benefits.

Sickness and Permanent Incapacity FAQ

The entire process should not take more than eight working days to finalise.

The process will take longer if additional information is required or if the standard forms have not been completed correctly. Submitting incomplete forms will lead to delays.

Sickness and Permanent Incapacity FAQ

Fully completed claim forms must be sent to [email protected].

Sickness and Permanent Incapacity FAQ

Additional medical information may be required to determine the progression of the medical condition, whether there are any complications with treatment and the prognosis. A general medical history questionnaire may also be requested. This could include an independent medical evaluation by a specialist chosen by PPS or an occupational therapy evaluation.

- There is a special claims protocol in place for the following conditions:

- Chronic pain.

- Chronic fatigue, tiredness or fatigue.

- Any psychiatric syndromes.

- Any cognitive impairment.

- Any inflammatory conditions of soft tissue.

- Vertigo, dizziness, loss of balance or tinnitus.

- Conditions that may have started prior to the business being granted, which could become chronic conditions or are already classified as such.

For claims related to these conditions, the assessor may ask for:

- Copies of clinical notes from the treating or usual doctor or the doctor who completed the medical reports at the time of application for the policy.

- The Mental and Behavioural Questionnaire (for psychiatric claims) completed by the doctor who booked the member off.

- A Medical History Questionnaire from the doctor who booked the member off for the following conditions:

a) Fibromyalgia, chronic fatigue syndrome (CFS), myalgic encephalomyelitis (ME) or post-viral fatigue.

b) Any condition related to CFS, connective tissue disorders, autoimmune diseases or ME. - The General Claims Questionnaire completed by the member.

- Additional information directly from the member or their treating doctor to support and finalise the claim.

- A consultation with a medical specialist in the relevant field, as requested by the assessor, to support the claim.

For any further questions about these conditions or the claims process, members are encouraged to refer to their policy documents or speak to their PPS-accredited financial adviser.

Sickness and Permanent Incapacity FAQ

If your claim period extends beyond the expected recovery time, PPS will request additional medical information from your treating doctor or specialist. This helps us understand why the recovery is taking longer. Based on the doctor’s clinical findings, we will assess how the illness continues to affect your ability to perform your usual professional duties and make an informed decision on the extended claim period.

Should the treating specialist/doctor have extended this period, the doctor will be asked to provide additional supporting information based on their medical examination. Based on this additional supporting information, PPS will be able to make an informed decision on the remainder of the claim period, considering the illness and its effect on your ability to perform your nominated profession.

Sickness and Permanent Incapacity FAQ

To enable PPS to manage claims and ensure that all valid claims are paid, the standard recovery times provide a guideline to assessors of what is considered a reasonable period to recover from a specific illness or procedure. The concept of "standard recovery time" considers current clinical practice and relevant medical literature in conjunction with PPS's claims experience. PPS will approve the sick-pay period, which aligns with current clinical practice.

Sickness and Permanent Incapacity FAQ

- A claim form completed by you (Declaration by Member form)

- A claim form completed by your treating doctor (Declaration by Doctor form)

- Proof of hospitalisation showing admission and discharge dates (front page of account or discharge form) for the Admission Rider and/or Family Responsibility Rider benefits.

- A marriage certificate, an unabridged birth certificate of the child and proof of medical aid for claims relating to your spouse or child.

- A copy of the official adoption court order and/or official proof of the registration of the adoption with the Registrar of Adoptions, a copy of the marriage certificate pertaining to the spouse and proof of medical aid for an adopted child.

- The respective benefit claim forms, completed by the member and the treating medical doctor, along with the unabridged birth certificate or proof of adoption papers, marriage certificate and death certificate (where applicable), for the Child Terminal Illness benefit.

Sickness and Permanent Incapacity FAQ

No, to claim the Admission Rider benefit you only have to be in hospital for four consecutive days (three consecutive nights) or more.

Sickness and Permanent Incapacity FAQ

When you are sick or injured and unable to perform any of your usual occupational duties due to that sickness or injury:

The S&PI product has two waiting periods, namely, seven or thirty days. Thus, depending on the waiting period you have chosen, the benefit will be paid as follows:

- Seven-day waiting period: A Total Sick Pay benefit will be considered if you were totally unable to perform any of your usual professional duties for at least seven consecutive days, due to sickness and will pay from day one retrospectively. Once this initial requirement for a minimum period of seven consecutive days of total incapacity is met, for the same or related condition, ongoing claims can be submitted for continuing total or partial claims. A partial claim is where if, after a valid total Sickness claim, the member can perform some of their usual professional duties but are still unable to carry out normal duties or work normal hours, PPS will pay the member a partial Sickness benefit (50%).

- 30-day waiting period: A Sick Pay benefit will be considered if you are unable, either totally or partially, to carry out your usual professional duties for at least 30 consecutive days due to sickness. The Sick Pay benefit will be paid on either a Total or a Partial basis, whichever is applicable, prospectively from day 31.

Please refer to your policy certificate to confirm if you have a seven or 30-day waiting period.

How To Claim

CLAIMS

Tell: 0860 777 784

Monday - Friday

24/7

HOME AND ROADSIDE ASSIST (EMERGENCY SERVICES)

Tell: 0860 777 784

24/7

CLAIMS:

1. All claims must be reported within 30 days of the incident

2. In the case of motor vehicle accidents, notify SAPS within 24 hours of the event

3. In the event of any crime related incident (e.g. theft), report this to the SAPS as soon as possible

4. The Claims Consultants will assist you regarding any further requirements

How To Claim

Follow the easy steps below to get your claim processed fast and efficiently:

1. FILL IN THE CLAIM FORMS

Claims for benefits in terms of the PPS Provider™ Policy should be submitted as soon as possible after the occurrence of the event that gave rise to the claim to ensure efficient claims processing. Claims will only be assessed for the period for which you are claiming, as reflected in the Declaration by Member form. Claims for future dates will only be assessed up to the date the Declaration by Member form is signed. For ongoing claims, claim forms should be submitted on a monthly basis, signed and submitted by the 25th of each month. Click on the relevant benefit tab on the left menu for the claim forms.

2. SUBMIT DOCUMENTS

You will need to submit all the requested claim forms and supporting documents to [email protected]. To assist you, please refer to the FAQ's or the relevant benefit tab on the left menu.

3.WE WILL CONTACT YOU TO NOTIFY YOU OF THE OUTCOME OF YOUR CLAIM

FOR CLAIMS CALL: 010 085 3820

Claims

You can send an email to [email protected];

Alternately contact PPS on 010 085 3820.

Claims

Yes, you may. Your application will be subject to the standard PPS underwriting policy and PPS will consider the information relating to the claim submitted. In some instances, such an application may be deferred for a period of time depending on the medical condition you are claiming for. The PPS Underwriting Department will communicate this to you.

Claims

The benefit will be paid to your premium-paying account once the claim is assessed and accepted as valid.

You may request PPS to pay the benefit to a different account. In such cases, you will have to provide PPS with proof of the account (a bank letter not older than three months). Please note that this will delay the payment of the benefit as due diligence of the preferred account will first have to be completed.

Claims

If you are not satisfied with the assessment of your claim, you may lodge a complaint by following the process as set out on the PPS website at www.pps.co.za/contact-pps. Click on the COMPLIMENTS/COMPLAINTS tab to download the document outlining the procedure.

Claims

No, it will not affect either.

Claims

Claims for benefits in terms of the PPS Provider™ Policy should be submitted within six months after the occurrence of the event that gave rise to the claim to ensure efficient claims processing. For ongoing claims, claim forms should be submitted on a monthly basis, signed and submitted by the 25th of each month.

Claims

All documents, irrespective of the content, are handled as confidential. However, you can advise PPS on your claim form to keep your PPS-accredited financial adviser informed. This does require your specific consent. If no consent is received, your adviser will not be informed regarding the progress of your claim.

Claims

Fully completed claim forms must be sent to [email protected].

Claims

You will be required to pay for the completion of the Declaration by Doctor Form. Some practitioners may require payment to complete this form. PPS will pay for any additional reports we request from your doctor.

Claims

Yes, you will be notified via e-mail or phone according to your preferred method of communication.

Claims

Possibly. Additional information may be requested from you or your (or spouse or child) treating doctor once assessed by a claims assessor, especially if the claim period exceeds the number of days the illness is expected to last or with particular conditions claimed.

Claims

Approved medical practitioners must have a minimum qualification of the following:

- BCh – Bachelor of Surgery

- BChir – Bachelor of Surgery

- BM – Bachelor of Medicine

- BS – Bachelor of Surgery

- ChB – Bachelor of Surgery

- DCh – Doctor of Surgery

- DS – Doctor of Surgery

- MBBCh – Bachelor of Medicine and Bachelor of Surgery

- MBBS – Bachelor of Medicine and Bachelor of Surgery

- MBChB – Bachelor of Medicine and Bachelor of Surgery

- MD – Doctor of Medicine

- BDS – Bachelor of Dental Surgery

- BChD – Bachelor of Dental Surgery

- DDS – Doctor of Dental Surgery

- DMD – Doctor of Dental Medicine

Claims

- A medical practitioner registered with the Health Professions Council of SA (HPCSA) or equivalent medical body outside South Africa and approved by PPS.

- A dental practitioner registered with the Health Professions Council of SA (HPCSA) or equivalent medical body outside South Africa and approved by PPS for dental-related claims.

- No Declaration by Doctor form completed by a chiropractor, homoeopath or psychologist will be accepted.

Claims

- All claim forms are available at www.pps.co.za/claims, under each product tab.

- E-mail [email protected] to request claim forms.

- Ask your broker to assist.

https://www.pps.co.za/faqs/all