Business planning: Mitigation in an era of unprecedented uncertainty

Risk planning and risk mitigation has always been a crucial part of business planning. However, navigating the current environment of business risks can prove to be challenging as business owners are now more anxious about business sustainability.

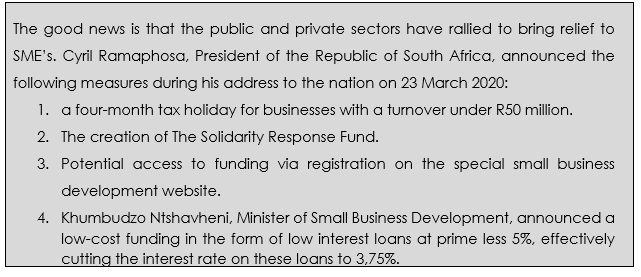

The impact of COVID-19 on Small and medium-sized enterprises (SME) cannot be overstated. SME’s do not have access to the large capital reserves, which large companies do.

Risks facing business and its owners

Risks such as a global pandemic do not come around as often as the typical types of risks that SME’s or large businesses face on a regular basis. However, whether risks present uncertainty or unprecedented uncertainty, business owners should always plan for liquidity and personal risks they may experience.

Liquidity risks

Liquidity risk is the inability of a business to service its short and long-term obligations, which affects its solvency over the long-term and liquidity over the short-term. With the current outbreak of Covid-19, short-term liquidity is one of the biggest risks facing business owners. Possible methods of addressing short-term liquidity risks are by improving cashflow and increasing current assets.

SME’s may consider decreasing its accounts receivable period by offering settlement discounts and negotiating extended accounts payable periods with suppliers. In addition, short-term low risk investments can enhance liquidity and current assets by providing access to capital and generating additional revenue in the form of interest. SME’s may also consider disposing non-income generating assets to improve their cash holding.

Likewise, short to medium term risks like the loss of a key person can be devastating for the business. Fortunately, this risk is an insurable one that can easily be mitigated.

Liquidity risk mitigation over the longer term can assist business owners in the event of death, ill health or infirmity. The creation of a buy and sell agreement funded by insurance addresses this risk. It provides the owners with certainty by providing an obligation for the surviving owners to purchase the business interest at a set price. The use of insurance makes it an extremely cost-effective option.

Personal risks

Personal risks include personal liability risks if an owner stood surety for a loan made to the business by a third-party. Some liability risks are inherent in the company structure. Owners and directors of a personal liability company (an Incorporated or Inc.) are held personally liable for the debts incurred by the company. An example of this would be a group of auditors who started a professional practice using a personal liability company structure. This scenario places the owner’s assets at risk. Possible mitigations include the creation of appropriate structures such as a trust to hold the owner’s personal assets and risk transfer in the form of an insurance policy.

Ensuring sufficient risk mitigation strategies

Business planning and sufficient risk mitigation strategies are best addressed by teams of cross-functional professionals skilled in understanding law, finance and financial planning. Lawyers help ensure that the agreements drafted are legally feasible and enforceable, finance professionals for appropriate valuations and cashflow management and financial planning professionals for comprehensive business needs analyses and advice on appropriate business mitigation strategies and solutions.

PPS Specialist Support Services provides expert advice and support in the fields of business, estate, investment and retirement planning. We offer a tax administration service too. Please contact your PPS accredited adviser or broker to schedule a virtual consultation with us. We are fully operational during the lockdown.

By Marlon Goss CFP®, Head of Specialist Support Services and Tamsyn Gradwell CFP®, Technical Specialist: Planning Strategist at PPS

PPS is an authorised FSP

https://www.pps.co.za/business-planning-mitigation-era-unprecedented-uncertainty