Do well-diversified portfolios translate to consistent returns?

Balanced funds – or multi-asset funds – combine bonds, money market instruments, equities and real estate in a single fund. Equities – considered a high-return but high-risk asset class – are included in portfolios for their inflation-beating abilities. In contrast, bonds and money market instruments are included for risk reduction and income generation. Multi-asset funds are considered to be well-diversified across asset classes, offering both income generation and capital appreciation, depending on the balance of income and growth asset classes.

How ASISA classifications serve as a guideline for risk exposure

Typically, the fund manager determines this balance based on the fund’s objective. However, the Association for Savings and Investment South Africa (ASISA) offers some guidance in its classification system. Multi-asset funds aiming to provide capital growth over the long term with low short-term risk are classified as multi-asset low equity funds. They can have a maximum equity exposure of 40%, maximum property exposure of 25%, and a maximum allocation of 45% to offshore assets, which increased to 30% in February 2022.

But does easy access to a well-diversified portfolio through a multi-asset low fund translate to consistent performance?

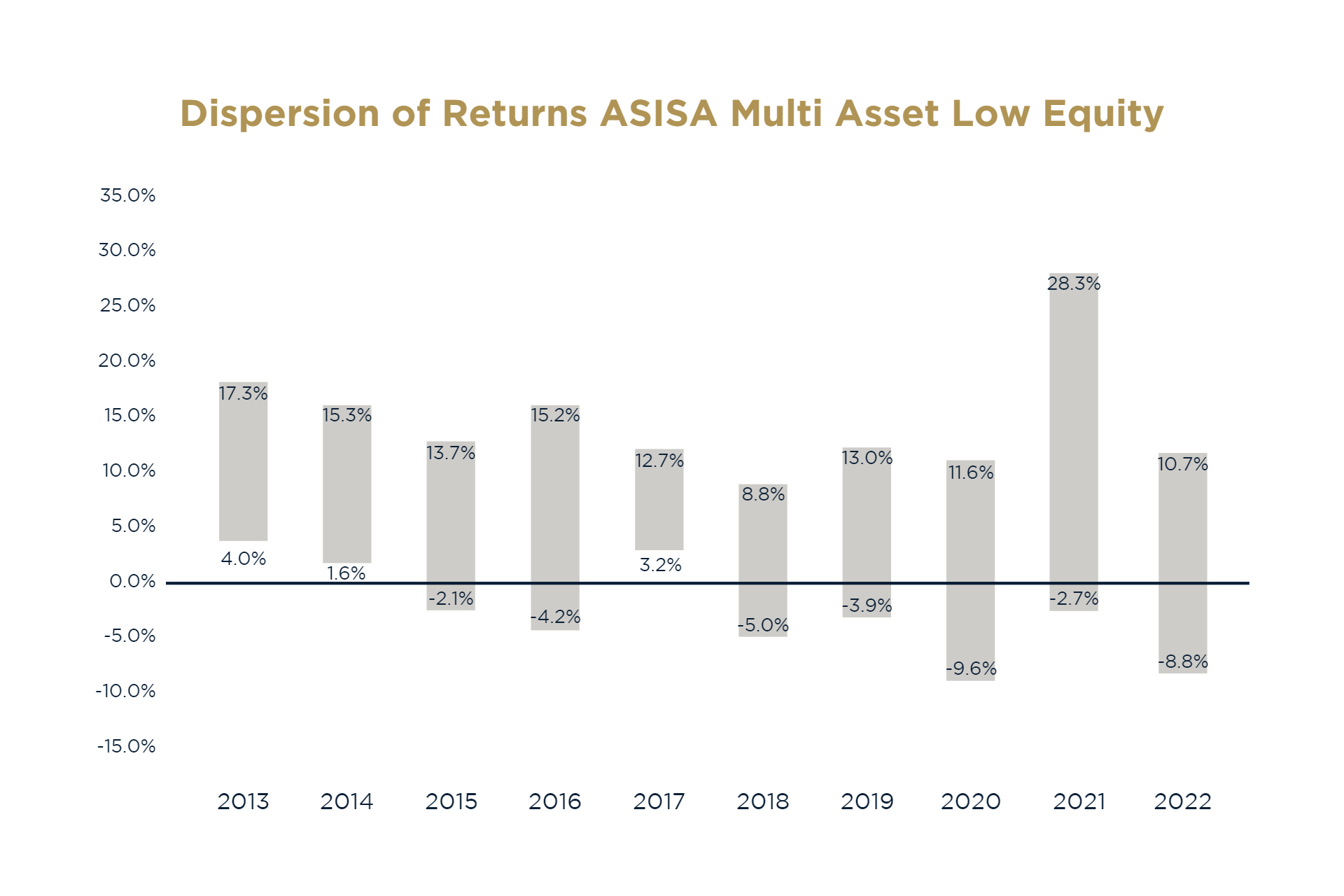

To answer this question, we looked at the dispersion of net fee returns for all the funds in the (ASISA) multi-asset low equity category over the last ten years. The results show that the dispersion of returns was wide for each calendar year and ranged between 9.5% in 2017 and 31.1% in 2021. For example, in 2020, the dispersion was 21%, with the best-performing fund returning 11.6% and the worst performing -9.6%.

Source: Morningstar

Focusing on 2021, which had the widest dispersion of returns, risky assets shot the lights out. In general, local and offshore equities and small capitalisation JSE shares significantly outperformed the more defensive asset classes, such as bonds and cash (both locally and offshore). Funds that tended to be defensively positioned from an asset allocation perspective lagged their peers.

2015 was the worst year for local bonds, which returned -3.9% when then finance minister, Nhlanhla Nene, was dismissed and replaced with a politically motivated individual, a move that sent negative market sentiment.

As a result, the rand weakened by 34% and funds with more offshore, relative to local exposure, outperformed their peers in the MA low-equity category. Within local equities, funds with exposure to the largest shares on the JSE and those that avoided resource shares – which were down 37% – fared much better.

2022 was unique in that bonds were as volatile as equities, driven by the fastest interest rate-hike cycle in history, along with global equities and bonds showing negative returns. This brought their traditional role as an equity diversifier into question. 2022 saw global cash and select local equities, resource shares and small capitalisation JSE shares drive performance.

What is clear from this analysis is that offshore assets have had a material impact on the dispersion of returns, an asset allocation call. Moreover, the increased offshore allowance will result in a wider dispersion of returns going forward. Additionally, a category with low equity exposure and high conviction equity views – whether in resources or small capitalisation shares – will tend to significantly impact whether a fund leads or lags from a performance perspective. Another factor that could determine a fund’s performance is the duration or interest rate risk.

While one cannot predict the markets, understanding a fund manager’s strategy and portfolio construction can provide insights into how they could perform throughout market cycles. This knowledge can only be attained through thorough research and rigorous assessment of the fund manager’s investment philosophy, approach and risk management as reflected in their portfolios.

In conclusion, having access to a well-diversified portfolio is not enough to guarantee consistent performance. A manager’s investment style will influence how they allocate to the different asset classes, the type of equities they invest in and stock selection. A more consistent performance could be achieved by selecting best-in-class fund managers within a particular style and blending fund managers with different styles.

By Laurette Ndzanga: Research Analyst at PPS Investments

PPS Investments is a lisenced FSP.

Business Brief Articles

https://www.pps.co.za/business-brief/do-well-diversified-portfolios-translate-consistent-returns