SECURING AND GROWING YOUR LEGACY

The notion of legacy is often referred to as something of the past. “My late mother’s legacy” or “Trump’s legacy of zero-tolerance on irregular border crossings”. In Alan Weiss’s, best-selling Your Legacy is Now he puts it eloquently that “But the thought that legacy arrives at the end of life is as ridiculous as someone who decides to sell a business and tries to increase its valuation the day prior. Legacy is now. Legacy is daily. Every day we create the next page in our lives, but the question becomes who is writing it and what’s being written. Is someone else creating our legacy? Or are we, ourselves, simply writing the same page repeatedly? Or do we leave it blank?”

Securing your legacy

The idea of creating your legacy every day by the choices we make is inspiring. It makes us consider ideas and opportunities with less complacency. It encourages us not to be lethargic in our approach to life, love and living. This theme of “taking action” must then also apply to securing the legacy we create. The Master of the High Court estimates that up to 70% of working South African’s do not have a Will. Are you aware of the specific events that will be put into motion should you die? Just recently, I asked my friends at a social event “who has a will?”. Even though they all understood the importance of having a Will, I was astonished that only two out of ten did. Several of my clients have a Will, but they are not always updated, and the process and procedures that will occur on their death have not always been communicated with their families.

Death is tragic, and the most significant gift we can leave is a legacy to be proud of and the certainty that all financial matters have been addressed and dealt with. Wealth planning for the future of one’s legacy is daunting, complex and difficult to face. Planning for after your death is not a comfortable topic to address and certainly not a topic brought up daily. In saying this, these issues aligned with leaving a legacy are far easier to avoid than address.

What to consider when securing your legacy

- Make sure your Will is updated.

- To avoid family feuds or dying intestate, it is important to make sure your Will is updated. It is not a once-off event and needs to be updated every time you have significant changes in your financial circumstances i.e. getting married, buying a house, retiring, getting children, parents passing away, changing jobs, etc.

- If you have an interest in a business, it is important that you have the proper buy and sell agreements in place. This protects your business partner and ensures that your dependents are not left with running a business when you are gone.

- If you have offshore assets, ensure a Will covers them in the necessary jurisdiction as your South African Will does not necessarily cover these.

- Do not forget the “soft stuff”. Often people want to pass down a philanthropic venture they were involved in. Even being an organ donor or having a strong conviction about cremation vs burial, and where possible list it all – do not leave it to chance.

- Make sure debt is covered and settled.

- Not only does debt repayments put an enormous strain on cash flow in your living years, but unsettled debt is also the quickest way of wiping away your legacy. Are these covered through a life cover policy or do you have a plan of settling them at your death?

- Many people do not ensure they have enough liquidity to settle any debts, costs or obligations at death. They need to remember that the South African Revenue Service has first claim to the estate and if there is not enough cash available, the executor will have no choice but to realise assets in the estate, potentially leaving beneficiaries in a compromised position.

- The effect of Tax.

- Death and taxes – the only two sure things in life (and after that). Structure your estate optimally and with consideration.

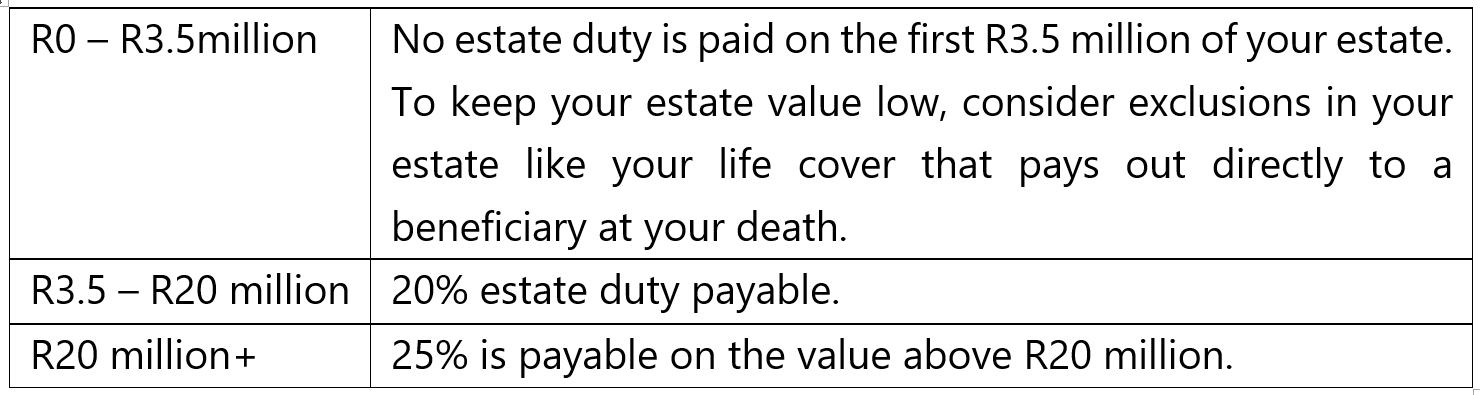

- Death is regarded as a capital gains event and your estate will therefore be liable to capital gains tax (CGT) before any gains are distributed to your dependents. There is a capital gain exclusion of R300 000 in the year of death and any assets bequeathed to your surviving spouse are also free from CGT, as are any bequests made to approved public benefit organisations. The proceeds of life assurance policies, benefits from retirement funds and money housed in living annuities are all exempt from CGT. That is why it is important to update your beneficiaries on these products and within your Will.

- Executor

- To ensure emotions are kept out of the decision-making process and to protect your family from stress or any unnecessary conflict, a reputable entity such as a trust/insurance company, bank or lawyer should be appointed as executor of your estate. If you want to add a family member, consider adding them as a co-executor.

- When setting up your Will, consider what assets could be kept outside of your estate so that it will not attract executor’s fees.

Growing your legacy

Growing and building a legacy are two separate things to me. Building our legacy is about creating that next page each day – with the choices we make and the meaning we create. Growing our legacy is how wise we are with our resources, ensuring our investments are well-positioned for maximum growth. When I meet with my clients, I make sure we do not only plan for death in isolation but a complete financial analysis for death, disability, critical illness, retirement and growing their financial portfolio by investing.

What to consider when growing your legacy

- Planning

- Each individual is different and accelerating your wealth requires a niche and highly personalised boutique proposition. An analysis of your financial status needs to be done, and a financial plan developed that is aligned to your financial and lifestyle objectives. You work hard for your money, and it is essential to make sure that it is working hard for you.

- Retirement is a crucial element of a financial plan. The rule of thumb is to save a minimum of 15% of your monthly income for your whole working life, which averages 40 years.

- Diversification

- My advice is never to concentrate your money or assets in one opportunity, but rather to diversify to reduce risk. Too much property may leave very little liquidity in your portfolio; too much cash means you are not beating inflation. A well-diversified portfolio split across companies, countries, assets and asset classes is always my recommendation.

- An excellent way to diversify is through offshore investing. A portfolio that includes offshore, holds stocks and securities that are not limited to South Africa. It offers the opportunity to diversify your portfolio by hedging against the rand and accessing the global equity market universe. There are various ways of investing offshore, but the two popular methods are through rand-denominated offshore funds or direct offshore investment in a foreign currency.

Like a road map, a fully comprehensive financial plan that includes your estate plan and Will becomes the foundation for establishing and implementing your legacy.

It is essential to walk the path with professionals. It is always useful consulting with an expert who can assist you in navigating the investment landscape. PPS Wealth Managers are here to help ensure your portfolio is structured in a well-diversified manner, and the funds’ allocation is optimal to meet your long-term goals.

By Werner Rossouw, PPS Wealth Manager

Kindly note that this article does not constitute financial advice; the information provided is purely informational. In terms of the Financial Advisory and Intermediary Services Act, an FSP should not provide advice to investors without an appropriate risk analysis and thorough examination of a client’s particular financial situation. The information, opinions and any communication from PPS Insurance, whether written, oral or implied are expressed in good faith and not intended as investment advice, neither do they constitute an offer or solicitation in any manner. PPS is a licensed Insurer and authorised FSP (FSP 1044).

Wealth Advisory Newsletter

newsletter region

https://www.pps.co.za/newsletters/what-pps-has-say-securing-and-growing-your-legacy