Implications of emigrating your money

The lure of a better quality of life, economic prospects as well as being closer to family and friends has resulted in many considering emigrating. Did you know that although emigration involves physically relocating from one country to another country, you do not need to necessarily financially emigrate when doing so? Financial emigration is when a taxpayer changes their status with the South African Reserve Bank (SARB) from resident to non-resident. This is a declaration that you will permanently leave South Africa and meet the requirements of being a non-resident for tax purposes. You will need to pay an exit tax to the South African Revenue Service (SARS) based on your worldwide assets.

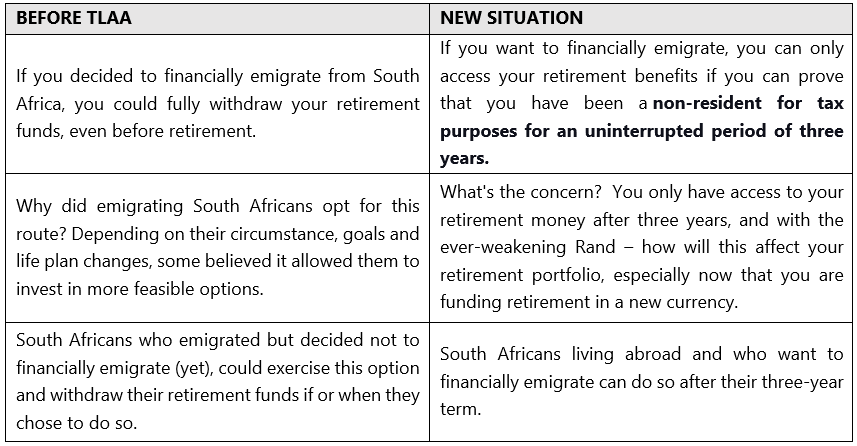

In the 2020/2021 budget speech, Finance Minister Tito Mboweni spoke about relaxing regulation around exchange control which had the high net worth market segment particularly excited. This, however, did not realise as President Cyril Ramaphosa signed the Taxation Laws Amendment Act (TLAA) into law in March 2021, which introduced fundamental changes to retirement and emigration.

A high-level overview of the effect of TLAA on South Africans

Should you pass away within the three-year term and your beneficiaries are abroad with you, funds can be paid to a non-resident bank account in South Africa and the retirement lump-sum tax-table would be applied in this instance.

What has everyone so concerned?

There is concern regarding what is believed as protracted political and economic uncertainty in South Africa. I have experienced high-net worth South Africans looking for a “Plan B” and evaluating countries like Portugal with their golf courses and restaurant price index of 41.56 (less than half of London’s 89.04) according to Numbeo.com’s cost of living statistics. Cyprus is another famous retirement tax haven or, of course, going to countries where people’s children have already emigrated to.

South Africans can take a tax-free lump sum when they retire with the first R500 000 not taxed. Anything more, is taxed at incremental rates: the next R200 000 taxed at 18%, the next R350 000 at 27%, and anything after that at 36% based on SARS’s retirement lump-sum benefit table. If you were thinking of emigrating to Portugal, lisbob.net explains how tax is levied at 10% on foreign pension to Non-Habitual Residents (NHR) during the first ten years of living there. However, your money is now locked in South Africa for an additional three years. In Cyprus, you are given a choice of paying either a flat tax rate of 5% on pension income over €3 420 (around R61 142) or the regular scaling rates, meaning you can make a decision that benefits you, according to expertsforexpats.com. Our South African 36% may seem high in comparison, but this has remained stagnant for some time, and the concern is that the SARB may evaluate this.

A further concern is the implementation of Wealth Tax. According to the World Inequality Report, the most affluent 1% of the population owns 55% of the personal wealth. Following the recommendations of the Davis Tax Committee, SARS will focus on consolidating wealth data for taxpayers through third-party information. According to South Africa’s National Treasury, this will help broaden the tax base, improve tax compliance, and assess the feasibility of a wealth tax.

What to consider

Firstly, if you want to emigrate, it is critical that you seek comprehensive income tax advice. It would be best to speak with your tax practitioner in South Africa and a tax professional in the country you want to emigrate to. In some countries, you are “deemed” a tax resident on the day you arrive, so your assets, foreign (e.g. South Africa) and domestic (in the new country you are in), are taxable. If you still have investments in South Africa, for example, a home that you are renting out, this could have significant tax implications if you decide to sell. It is essential to consider that exit Capital Gains Tax (CGT) could be applied on assets as a deemed disposal when you break your tax residency, even if those assets are not necessarily disposed of at that time. Different countries have different rules, and it is crucial to get expert advice on this matter. Understanding the tax residency rules for the country you are emigrating to is critical to ensure your financial health.

Secondly, your age at the time of withdrawing your pension. If, for example, you withdrew R8 million (after your three-year waiting period), you would pay in the region of R2,8 million in **tax. If you waited until retirement, you would pay around R2.6 million on an R8 million *withdrawal, effectively saving in the region of almost R200 000. So, if you are in your thirties, you may opt to pay the higher tax rate and make the withdrawal, as you may have concerns that the tax rates could change by the time you retire, and perhaps you believe you have enough time to make up the difference and invest your balance in a currency that you think will appreciate over time.

Thirdly, you may opt to take a third of the fund value in cash and use a South African living annuity, but only if this makes sense from a tax point of view. Living annuities do not have to comply with regulation 28 like pre-retirement funds, and you could invest the underlying assets in international feeder funds that would have virtually no South African holdings, effectively taking the risk of Rand volatility off the table. You can channel this income directly into an offshore bank account. So, this could be a viable option for some. However, you would need to understand the double tax agreement between South Africa and your country of tax residence on the lump sum and the living annuity income.

Whatever you are considering and wherever you decide, it is essential to walk the path with professionals. Treasury has instated a dedicated unit in SARS, ensuring that wealthy individuals with complex financial structures pay Caesar what is due. We need to ensure that our financial matters are 100% above board, so make sure you receive the best advice possible, no matter whether you’re staying or going.

by PPS Regional General Manager, Tango Gatya

* https://www.sars.gov.za/Tax-Rates/Income-Tax/Pages/Retirement-Lump-Sum-Benefits.aspx

**https://www.sars.gov.za/Tax-Rates/Income-Tax/Pages/Rates%20of%20Tax%20for%20Individuals.aspx

Kindly note that this article does not constitute financial advice; the information provided is purely informational. In terms of the Financial Advisory and Intermediary Services Act, an FSP should not provide advice to investors without an appropriate risk analysis and thorough examination of a client’s particular financial situation. The information, opinions and any communication from PPS Insurance, whether written, oral or implied are expressed in good faith and not intended as investment advice, neither do they constitute an offer or solicitation in any manner. PPS is a Licensed Insurer and Financial Services Provider (FSP 1044).

Wealth Advisory Newsletter

newsletter region

https://www.pps.co.za/newsletters/what-pps-has-say-implications-emigrating-your-money