Article Name

Making sense of investment cycles

Published: August 1, 2022

Equity markets have been under considerable selling pressure in 2022, as investors anticipate that stubbornly high inflation will cause central banks to raise short-term interest rates multiple times this year. At the same time, expectations for global economic growth have been revised downwards, following further disruptions to global supply chains on the back of Russia’s invasion of Ukraine and China’s strict COVID-19 lockdown measures.

When investing for the long-term, it’s helpful to remind oneself that while markets go through cycles, and it is often more important to focus on the long-term trend than become preoccupied with the short-term fluctuations. As a multi-manager, the critical questions for us are whether interest rates, inflation and economic growth are likely to be structurally higher or lower, than we have assumed in the past. These questions are important because it will impact on both our long-term strategic asset allocation to the various asset classes, as well as whether tactically we are receiving sufficient compensation to overweight or underweight a particular asset class.

Currently, financial markets are pricing in substantial short-term interest rate increases from central banks (the South African Reserve Bank (SARB) this year is expected to hike by 0.5% a further 6 times after May and the US Federal Reserve (Fed) 4 times), but these rate hikes are coming from multi-decade low starting points, and markets have not materially upwardly revised their long-term expectations for the neutral short-term interest rates of around 2.5% for the Fed and 7.5% for the SARB.

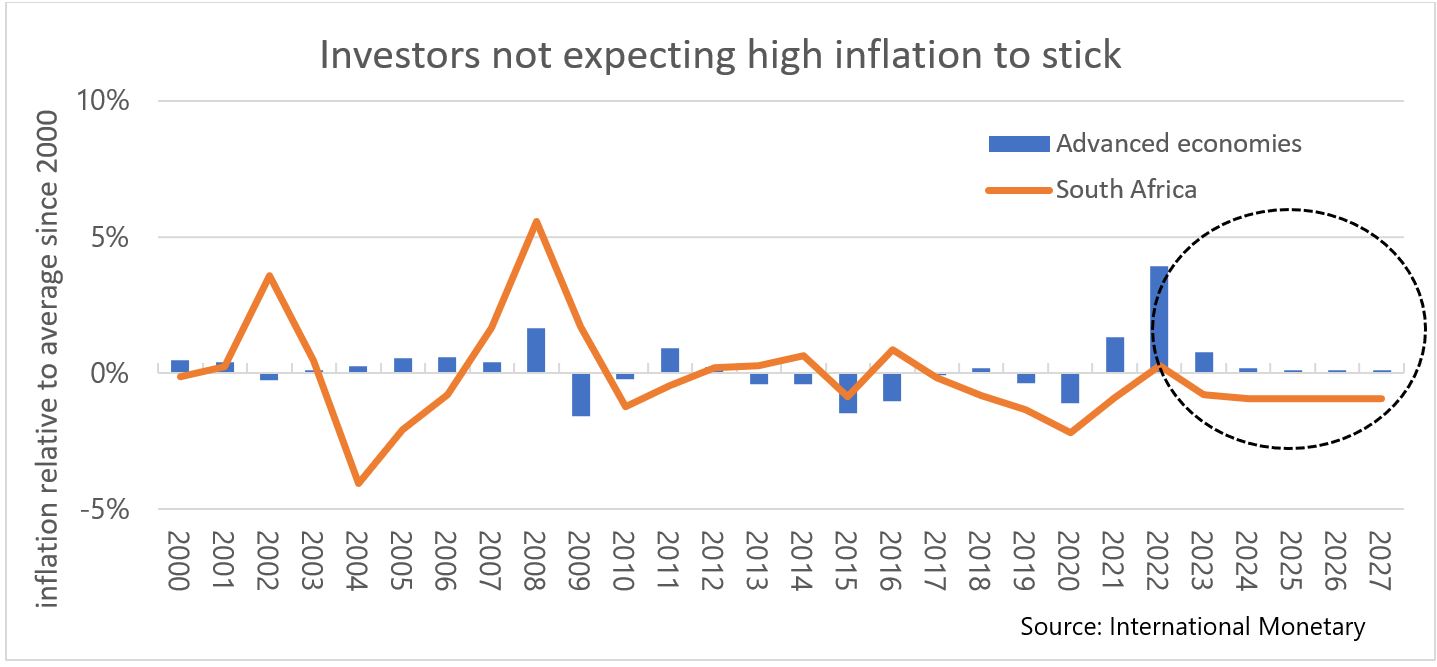

Long-term inflation expectations today are still anchored around what they have averaged since 2000. The International Monetary Fund forecasts that developed market inflation may be back below 2% p.a. by 2024 (it has averaged 1.9% since 2000) and is not expecting South African inflation to exceed 6% p.a. over its forecast period (it has averaged 5.5% since 2000).

Consequently, while the market is preoccupied with the latest (high) inflation number, the critical decision is not so much the speed that inflation reverts to its trend (although this is clearly an immediate and pressing concern), but rather whether the trend for inflation over the next couple of decades will be similar or structurally higher than it was in the past.

Given that markets are not expecting long-term structurally higher inflation, our portfolios tend to have a strategic allocation to inflation-linked bonds, as they will offer some protection should inflation be closer to the 5% it averaged for advanced economies (and more than 10% for South Africa) in the twenty years preceding 2000.

At the same time, we have started building up a higher cash position, given the market is not anticipating that real interest rates could be materially higher than the recent past, with muted interest rate expectations more than twelve months out.

While the prospect of an economic recession will undoubtedly have an impact on asset prices in the short-term, the more important question for the next decade (or two) is whether the global economy will continue to grow at its historical trend growth of 3.5% p.a. through its transition to a greener economy, and whether the SA economy will remain structurally stuck in an underwhelming 1% p.a. growth rate for the foreseeable future.

Our portfolios have an overweight to SA assets, as we believe we are receiving sufficient compensation for taking on the risk of mediocre economic growth, given the market is not expecting that South Africa will be able to implement the reforms to change its growth trajectory in a positive direction.

At the same time, and partly to diversify this SA specific risk, we have a long-term preference to (global) asset managers who can include a growth focus, given our view that such managers are more likely to identify companies that will benefit from the global transition to a less carbon-intensive global economy, while also favouring strategies that are flexible enough to include value opportunities should it make sense.

In short, it is tempting to get swayed by the short-term noise around economic variables and try to anticipate their next direction. But it is incredibly difficult to time investment cycles, and we think it is often more useful to look a bit further out rather than try to time short-term moves.

Our portfolios try to look through short-term volatility, to appropriately benefit from longer term trends, while remaining well-diversified to limit short-term volatility.

By David Crosoer, Chief Investment Officer at PPS Investments

https://www.pps.co.za/making-sense-investment-cycles